One day, I was enjoying a cup of coffee at a coffee shop in the greater Colombo area located on prime property. A gentleman joined me and we began a conversation. As we spoke, he mentioned he was actually the landlord of the building and had rented it out to someone else.

I asked: “Why are you renting this place? Isn’t it better for you to run this shop so you can earn a better return?” His response was: “Actually, I tried for two years and made a profit too.” I was surprised that renting it was more profitable than running a business.

I inquired about the reasons. He mentioned that he was making a profit of about Rs. 50,000 per month by running his own business and he could not exceed it. But by renting out the same building, he earns about Rs. 350,000 as the rent income.

The rest is not rocket science; when you have the capacity to earn Rs. 350,000, it doesn’t make any sense to settle for 50,000.

But in national economic issues, people often get carried away with just the profit without considering the asset value which generates that revenue.

Divesting of SOE shares

A recent case is the argument against divesting the majority shares of a State-owned telecom company and a hospital. Often, the argument is: “Why should the Government be selling the profit-making entities while the loss-making entities are the problem?”

Of course, the loss-making ones are the main problem, but the Government making a profit doesn’t really reflect whether that profit is worth it or not – as with the case of the landlord of the coffee shop. If the Government makes just Rs. 50,000 when the actual capacity is making Rs. 350,000 with a better purpose, it is in fact a loss of Rs. 300,000.

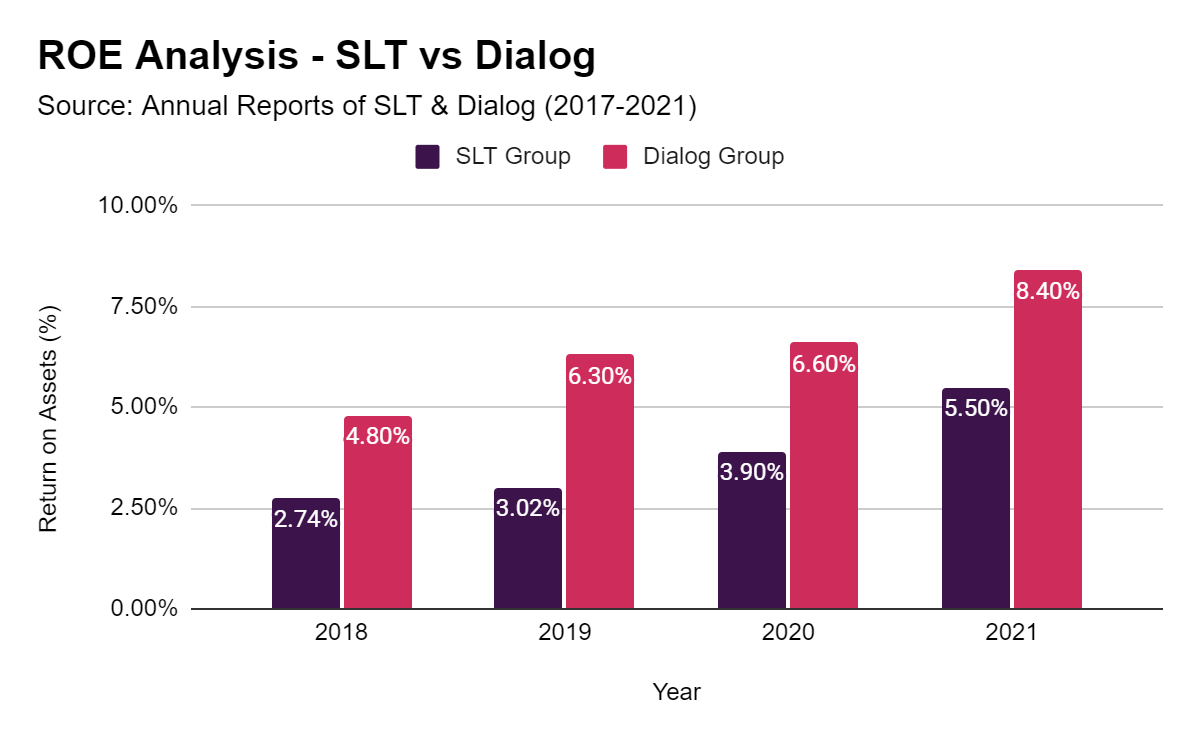

Many people are not aware of the fact that the Return on Assets (ROA) of the profit-making entities owned by the State is far less than the industry standard. Some are making profits simply by being a monopoly or getting preferential treatment from the Government. The value of the business has to be based on the value of assets it owns. In other words, what matters more is the profitability of the company in relation to its assets.

Motivation for profits

So when we compare the ROA of a Sri Lankan State-owned telecommunications company with the private sector telecommunications companies, it is evident that the State-owned telecom company has a lower ROA compared to private companies. It is not surprising because the motivation for profits comes with ownership.

When there is no owner and when it runs on taxpayer money spent by political appointees, there is no intention of maximising profits. In that structure, the incentive is for longer survival and absorption is reduced as much as possible.

It is a classic case similar to a farmer encroaching on forest land to yield more harvest without considering productivity in the long run. It is not the size of the harvest that matters but the harvest that can be obtained per unit of land. Similarly, it is not the profit gained but the profit in relation to a unit of assets.

On the other hand, we need to realise these losses have to be borne by taxpayers. That is one reason why the Government should not run any business. Even the ones which make profits can easily drift to loss making when governance structures are not in place. It has happened multiple times.

When we restructure SOEs, of course the first preference would be for profit-making ones. It’s not rocket science, since no one wants a loss-making entity. When someone takes a loss-making entity and if the entity has a high level of liabilities, those liabilities have to be absorbed by the Government – meaning, the people.

That is one reason why the Government should not engage with commercial operations because losses are borne by the citizens while the benefits of profits are not necessarily shared among the citizens.

Transparency and accountability key

In the process of reforming or divesting the assets of the State, it is of paramount importance to proceed the transactions on a competitive basis. One reason why people have suspicion over State asset divestments and privatisation is because the previous transactions had a lot of grey areas. Thus, the suspicion is obvious.

If the Government is committed to reforming State-Owned Enterprises (SOEs) and attracting the right type of investors, the only tool it has is transparency. Any bad transaction will backfire on the rest of the reforms, extending to even debt restructuring and bilateral support. We can only advise and play the role of watchdog – the people who have power should walk the talk.

(The writer is the Chief Executive Officer of Advocata Institute. He can be contacted via dhananath@advocata.org. The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute or anyone affiliated with the institute.)